{kind=link}

Financial inclusion has increasingly gained recognition as a pivotal driver of economic development, fostering empowerment and equitable national growth.

It goes beyond the mere accessibility of financial products; genuine financial inclusion necessitates the thoughtful design, seamless accessibility, and tailored responsiveness of these services to cater to the diverse needs of individuals and businesses.

In the context of the Philippines, a country teeming with potential yet grappling with persistent challenges, financial inclusion has taken centre stage as a catalyst for economic resilience and shared prosperity.

This spotlight on financial inclusion was particularly pronounced during the recently concluded INDX3.0 and 2023 Law x Tech Summit. The event deliberated and explored emerging technologies that have the potential to amplify inclusive innovations further.

Within this landscape of discussions, financial inclusion held a central place, reinforcing its paramount importance in the journey toward a more inclusive and digitally empowered society.

Navigating the complex terrain of financial inclusion

With a population exceeding 109 million, the Philippines is one of the most populous countries globally. This demographic landscape offers a unique opportunity for what is known as the demographic dividend—a period of accelerated economic growth driven by a youthful and productive workforce.

However, financial inclusion in the country is still impeded by economic, physical, and behavioural issues that need addressing.

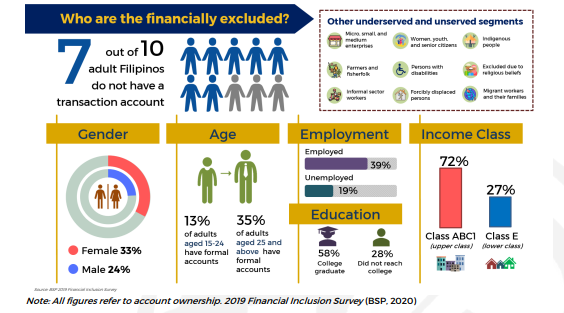

Account ownership accelerated in 2021, with a target of 70 percent in 2023. More than half of the borrowers have access to formal credit with 56 percent, while informal credit is 47 percent. The uptake of insurance and financial investment needs improvement.

The distribution of financial services across the archipelago remains uneven, driven by regional disparities. Urban centres such as the National Capital Region and Central Luzon enjoy better access to financial institutions.

At the same time, remote and less developed regions like the Bangsamoro Autonomous Region and Cordillera Administrative Region struggle to establish financial infrastructure. This geographical divide exacerbates the lack of basic amenities, including reliable roads, power supply, and internet connectivity, particularly in rural areas.

The nation’s susceptibility to climate change and natural disasters poses additional challenges, underscoring the need to cultivate financial resilience in sectors like agriculture.

The dawn of the digital era in finance

The digital revolution sweeping through the financial sector has ushered in a new era of opportunities for advancing financial inclusion. The rise of digital banks, fintech solutions, and online payment platforms has provided a means to bridge the accessibility gap.

The adoption of digital financial services (DFS) has surged, especially in response to the COVID-19 pandemic, which prompted a widespread shift toward online transactions.

A manifestation of this transformation is the doubling of digital payments‘ share in the retail payment landscape—a testament to the growing popularity of online transactions.

More Filipinos own mobile phones than have access to formal financial accounts, highlighting the untapped potential of mobile-based financial services.

Furthermore, the rollout of the Philippine Identification System (PhilSys), the national digital identity system, promises to address identity-related barriers and foster innovation in DFS. As of 11 July, over 80 million Filipinos are registered for the system.

BSP Deputy Director Mynard Bryan R. Mojica of the Financial Inclusion Office

In addition, the central bank is actively pursuing two distinct phases of digital financial inclusion. The first phase, Digital Financial Inclusion 1.0, is centred on establishing a robust digital payments ecosystem to facilitate the rapid uptake of account ownership and usage.

During the INDX3.0 and 2023 Law x Tech Summit, BSP Deputy Director Mynard Bryan R. Mojica of the Financial Inclusion Office said, “Harnessing the power of data through initiatives like PhilSys and the BSP’s open finance framework will be game changers for financial inclusion.

“Not only will they address account opening barriers, but they will also pave the way for greater innovation in digital financial services,” he added.

Complementing this, the second phase, referred to as Digital Financial Inclusion 2.0, focuses on constructing innovative platforms tailored to offer welfare-enhancing financial services, catering to the unique needs of every individual.

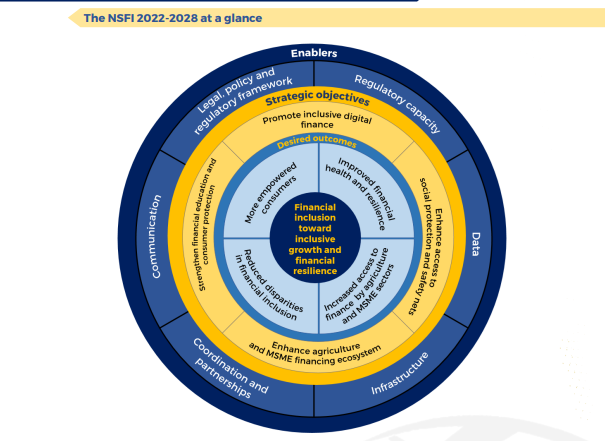

The pillars of the NSFI Strategy 2022 to 2028

The Philippines inaugurated the National Strategy for Financial Inclusion (NSFI) in 2015, acknowledging the evolving dynamics of financial inclusion in the digital age.

In 2022, a fresh iteration of the NSFI strategy was introduced, catering to emerging challenges and opportunities.

Mynard Bryan aptly highlighted that financial inclusion has increasingly gained recognition as a pivotal driver of economic development, fostering empowerment and equitable national growth.

“This recognition transcends accessibility, highlighting the imperative of thoughtful design, seamless accessibility, and tailored responsiveness to meet diverse needs”, he said.

The strategy hinges on four key outcomes – reducing disparities in financial inclusion, improving financial health and resilience, empowering financially capable consumers, and enhancing access to finance for MSMEs and the agriculture sector.

Firstly, the strategy aims to promote inclusive digital finance by creating a regulatory environment that embraces digital innovations, thereby ensuring the efficient delivery of financial services that are not only affordable and accessible but also customer-centric.

Secondly, strengthening financial education and consumer protection is a pivotal objective, with the strategy seeking to empower consumers through comprehensive financial literacy programs while reinforcing regulations that uphold ethical market conduct.

The NSFI strives to enhance access to risk protection and social safety nets, encompassing the development of robust mechanisms, both in the public and private sectors, to safeguard vulnerable segments from shocks and uncertainties, with an explicit focus on leveraging digital finance.

Finally, the strategy is committed to enhancing the agriculture and MSME financing ecosystem, aspiring to create a nurturing environment that attracts diverse players to engage with these sectors, bolstered by robust financial infrastructure and frameworks.

By augmenting access to financing for these sectors through initiatives like credit guarantees and secure transaction frameworks, the strategy aims to unlock their transformative potential.

Paving the way to shared prosperity

The NSFI strategy champions a conducive regulatory environment that stimulates diverse players to provide innovative financial services. It emphasises the pivotal role of comprehensive digital financial literacy programs and robust consumer protection mechanisms.

The strategy underscores the significance of government programs that foster financial resilience and safeguard the most vulnerable sections of society.

Mynard Bryan emphasised that the NSFI is more than just a strategy document; it serves as a platform for Bayanihan, the culture, to work together to achieve a shared goal.”

“Since financial inclusion is multidimensional, we need the support and cooperation of everyone,” he added.

The Philippines aims to overcome barriers and forge a resilient financial ecosystem through the comprehensive and multi-dimensional approach to financial inclusion encapsulated within the NSFI strategy.

The NSFI strategy is a blueprint for nurturing equitable growth, empowering individuals and enterprises, and constructing a more financially resilient nation.

With collaborative efforts, a commitment to innovation, and sustained endeavours, the Philippines’ vision of financial inclusion as a catalyst for shared prosperity takes tangible shape, promising a brighter future for every Filipino.